As I promised several times during this year, that we will close 2020 with a special issue of statistics. Without a doubt, it is time for me to fulfill this errand.

Here is a summary for those who don’t know much about INLOCK: INLOCK is a Hungarian crypto project which has launched at the end of 2017 and has an extensive service since the 16th of January, 2019 for almost 10.000 active clients, their number doubled in the past year… but let’s wait with the numbers. INLOCK launched as a social peer-to-peer lending platform, – tailored to market needs – although it oriented to managed services in 2020 and created the Savings Account besides the extant lending products.

First and foremost, a brief summary about what happened with the project in the last two years, then a demonstration about where are we now exactly:

History of the last two years

In April 2019, we launched peer-to-peer lending.

In May 2019, we won the special prize of the National Research, Development and Innovation Office.

During the summer of 2019, we reached 4000 users, who run almost 500 loan transactions and the amount handled by the platform has crossed the $ 1 million line.

In September 2019, we successfully listed the ILK token on the Liquid.com stock exchange, and it is available to exchange for BTC and ETH since then.

During the autumn of 2019, we presented INLOCK at numerous international and local conferences.

At the end of 2019, by identifying the market trends, we decided to modify the strategy. Instead of peer-to-peer services, we started to adapt so-called managed services.

In January 2020, we prepared INLOCK to comply with the newly released strong customer identification and AML processes in Hungary and the EU.

In February 2020, we successfully launched our first two managed services: “Stake” and “Managed Lending”.

In May 2020, we created significant marketing campaigns and participated in multiple conferences. Thanks to the activity, the number of users on the platform increased to 7500, in addition, because of the newly introduced managed services, the client assets managed by the platform have already reached $ 5 million.

In April 2020, we made a contract with Fireblocks, through which a dedicated insurance protects the client assets managed on the platform.

In the summer of 2020, INLOCK’s services became mature enough to start developing the mobile app, which also published on Android and iOS platforms.

By September 2020, we finished making the peer-to-peer services that were identified as a strategic goal and launched our “Savings Account” product, which is INLOCK’s most popular product to this day.

In November 2020, we started to plan the strategy for 2021. The most important point of this is creating the INLOCK White Label program, which leads the way for us to enter the B2B(2C) market in addition to our existing B2C business expansion, while significantly increasing the awareness and promotion of INLOCK with this.

In December 2020, the INLOCK Prime Program has launched!

Where are we now?

Based on the timeline above, it’s clear that 2020 was about pivoting for the INLOCK project, where we switched in two steps from the peer-to-peer model to the Savings Account product.

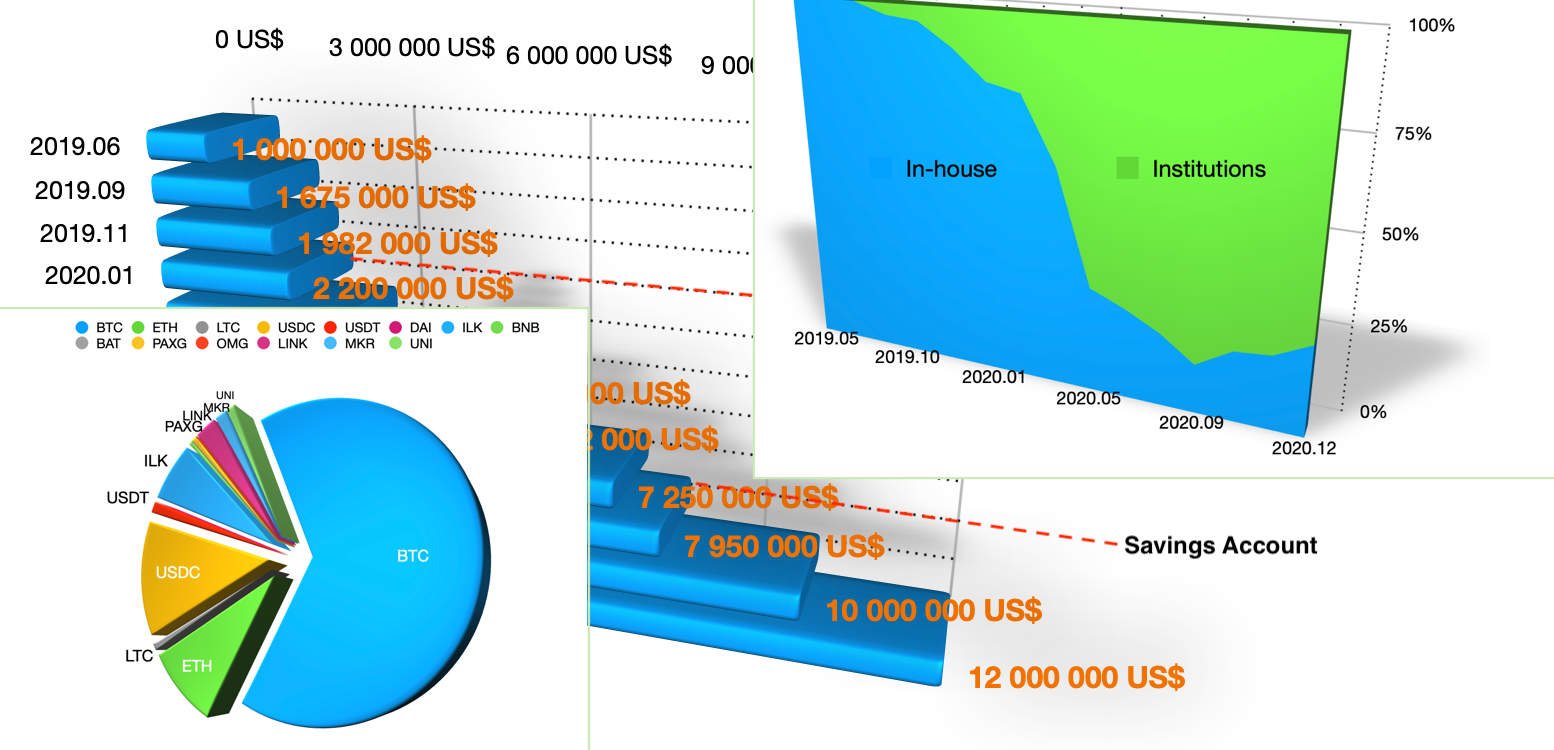

In parallel, the amount of crypto handled in the INLOCK platform has been continuously increasing. But how much and what effect did the introduction of the Savings Account product have on this?

It is clearly legible from the figure to what extent the transition to managed services has strengthened the acceptance and use of the platform.

Why did it matter so much? One of the main criticisms of crypto solutions is that they are too complicated, require a lot of attention, are complex and have terrible customer experience. Although I believe to this day, that there would be viability in the market for a solution like the one we created last year for the “ProLending” product… The fact that a couple of dozen users actually enjoyed using it in the fall of 2019, when they also simply reached 30-35 % of annual interest on a pro-rata basis. But the table above is a good example of how many more customers and assets we have gained from giving up market competition and instead, providing guaranteed weekly interest rates on deposits, for which we have increasingly reallocated interest income to our institutional clients.

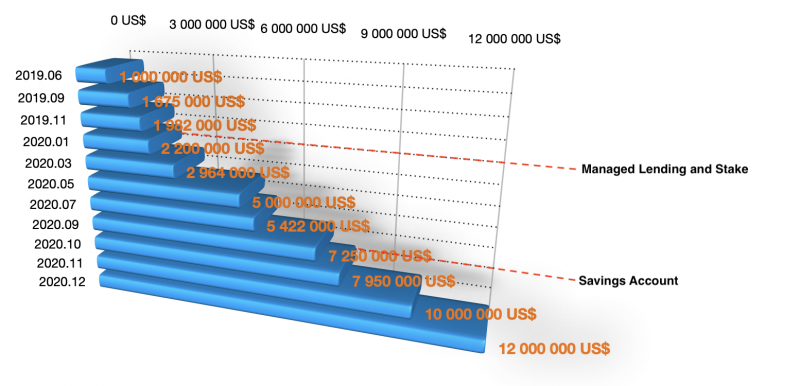

How did the ratio of in-house loans to institutional transactions turn out?

As seen above, we were able to manage the huge increase enormous quantity of assets mostly with institutional borrowers, but since September, the ratio of borrowing on the platform has started to strengthen, which can be explained by two phenomenons: on one hand, we announced several special offers for discounted interest rates before the holiday season and on the other, the world has turned and today it is no longer necessary to explain to anyone why it is worth taking out a loan for over-secured collateral… What matters is the fact that the exchange rate of Bitcoin and other leading cryptocurrencies has flew up in the skies in recent months! We can expect the rate to turn around again next year if the current positive market sentiment remains longer.

I recently wrote a more detailed article on institutional borrowers and the business relationship with them, find it on INLOCK”s Medium blog!

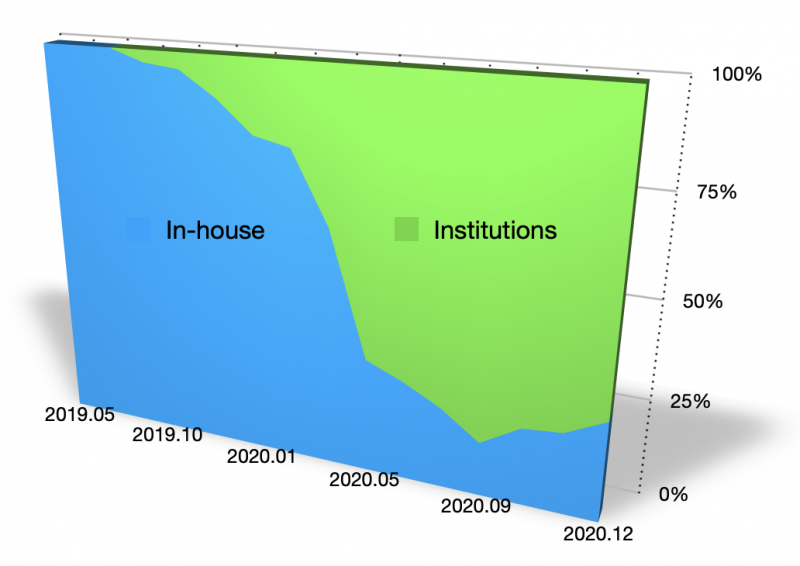

What exactly is this $12 million asset portfolio made up of?

Currently, INLOCK handles 14 different types of assets, the distribution of which can be read from the figure above based on their total dollar value. I don’t think anyone should be surprised about the almost 64% share of Bitcoin, as the “value-preserving” function of Bitcoin can be well combined with the INLOCK Savings Account function. They can go hand in hand. USDC takes the second place on the list, which accounts for 13% of the total managed assets, followed by Ethereum with 9% and the platform’s own native token, ILK, with a ratio of 6.4%. In the 1-2% range, USDT, Chainlink, MKR and UNI tokens compete.

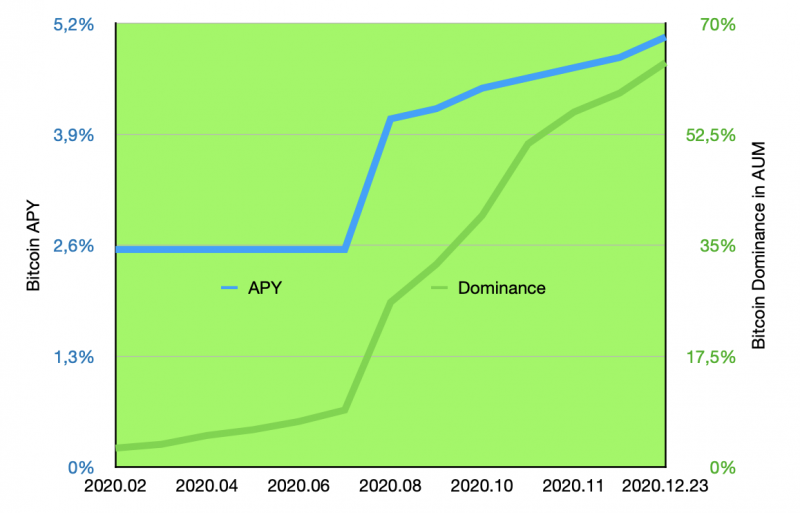

We get questions a lot about what makes the interest rates change. One of the most important coefficients is in the picture above. The larger the quantity we can take care of from a given asset category (e.g. Bitcoin, USDC, etc.), the more we can make good deals with market participants. We also have several institutional partners who are open to borrowing literally any coin from the Top100 list… but for less than $100,000 in total, they are simply not interested in making the business. To what extent the expansion of the supply can have a beneficial effect on the annual interest rate of each asset is perhaps best illustrated in the figure below:

Some good-to-know background information: although Bitcoin, as a tool was introduced to the INLOCK platform from the first moment (January 2019), up until February 2020, it could have only be used as collateral for a loan, accordingly its rate was not too high either. But that changed quickly when we introduced the Bitcoin Deposit option in February 2020 and then the Savings Account from September. It can be clearly seen that when Bitcoin began to flow into the platform, interest rates were able to rise steadily from an initial 2.55% to 5.04%.

Now that it is transparent what the asset portfolio managed by the platform looks like and how it affects interest rates, we can move on to customers.

We can take several interesting statistics on customers, but one of the most important of these is the measurability of the network effect in case of a product intended for the retail market. In the case of INLOCK, the “Pioneer Program” is designed to support this. Let’s look at the undisguised truth:

How much is it worth to use the Pioneer Program? Invitations were rewarded with $31,445 only in 2020! Our most enthusiastic Pioneer pocketed $5,212 in rewards, but the average reward reached $78 as well. All of this is due to the fact that INLOCK’s invitation program clearly offers outstanding rewards.

24,5% of INLOCK’s newly registered clients come from invitations!

This is typically not the number we should be proud of, but let’s dig a little deeper:

- 32,7% of the newly registered clients joined the platform as an invitee in 2020.

- 34% of the registered clients joined as an invitee since introducing the mobile app.

- 41% of the registered clients joined the platform as an invitee since introducing the Savings Account.

The trend is definitely increasing, which is a very important basis for showing a tangible network effect…, but it is clear that 2020 was more about finding a way than building an active customer base. Well, the year 2021 will bring a lot of changes! In addition to the Pioneer Program, another important component of customer acquisition and retention will make its new debut.

And how are we dealing with the country-wide distribution of the customer base?

42% of INLOCK’s active customer base comes from Hungary, which holds 60% of the total assets under management in INLOCK. Undoubtedly, the majority of customers are located in Hungary, which is why we considered it important in January 2020 to focus on strengthening and stabilizing the domestic user base rather than forcing a debut on the international stage. This strategy was basically accomplished, as our domestic numbers have grown, but thanks to the campaigns and the good reputation of INLOCK, we have also managed to achieve a number of more serious results on the international stage. Our second-largest customer base (nearly 10%) is from the United States, followed by the major European countries, Germany, Great Britain and Austria. Neighboring countries are also in a prominent position.

It is necessary to note that in the comparison, the classification was based on the nationality of each customer, and not on the basis of their address and country of residence. It is interesting that a significant part of our Hungarian clients lives abroad. Also, people over the age of 60 are actively transacting.

Of course, if we look at the ratio of the follower base not only for the active clients but also for the followers of the project, the situation is immediately different. For example, if I look at the weekly published interest rate newsletter, 12% of that is read in Hungarian and 82% in English.

We expect a bigger rearrangement in 2021 in terms of proportions within the categories, which will be facilitated mainly by the INLOCK White Label program.

On the bumpy road of renewal

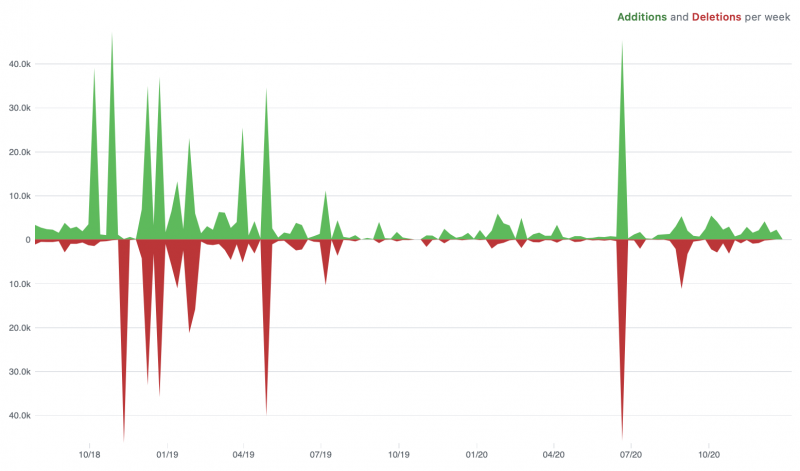

When a bigger company puts the word “renewal” in their mouth, it usually means that a desperate colleague who fears their job throws it in as an idea right in the middle of a marketing meeting, and somehow it gets into the ears of the management. Literal appearance renewal that looks good to customers, but god forbid we really want to stir up the real processes. I could talk for hours about why this isn’t such transparent bullshit at INLOCK, but I’m letting GitHub talk instead:

“The picture shows the “code frequency” diagram, which sounds quite good, but actually shows how much newly written code gets in a project and how much previously written code is thrown out on a pro-rata basis. Of course, the picture has its own particularities, which is why GitHub experts could debate about its relevance (e.g. how relocations prevail in such a figure), regardless, all the insane development that INLOCK has gone through this year can be seen from just the proportions too… It has actually meant the same amount of background work – invisible to customers – during which we retired a huge amount of previous features and code. This summer, we said goodbye to the ProLending feature for good, and then retired the Stake feature, which we actually introduced in January this year and whose sole purpose was to prepare for the debut of the Savings Account. In the first half of the year, several old codes were removed, such as Superposition, which was launched as a product last September, but until the beginning of this year, several customers still had contracts running, so we had to wait for them to run.

How good of a message does renewal mean?

A typical question is how good an advertisement is to take it anyway when a beginner startup talks about its tumbles and how they started again from almost zero. To understand the importance of this, you need to learn to think a bit like a startup. A phrase repeated to boredom is that out of 10 newly launched startups, 9 will almost certainly bleed in a few years before it can show significant results.

The reason for it all is what this phrase deals with less. While it is undoubtedly true that not everyone is an entrepreneur and many run out of enthusiasm or even their financial reserves sooner than they reach that certain “break-event” point.

So if we don’t handle it as a fact that 9 out of 10 people is incapable of being an entrepreneur, then there has to be a coefficient more important. This is nothing more than how the leaders of the business are earth-bound.

In 2017, we found INLOCK with infinite confidence, multiple hundreds of fully-written flipcharts, multiple hundreds of hours expended to planning, modeling, plenty of brainstorming, and we are already past the difficulty of the job with the team together. From here, we just have to do the miracle we planned, which will be definitely good… since we would use that with a very good heart. We couldn’t really explain to outsiders why it would be good and not even this fact could overshadow our blind belief! Most of our early token buyers declared openly that they didn’t buy a token because of the potential in INLOCK… much more because they see the imagination of the team at a level that they believe: we’re getting something out of it.

And we got to the answer here: The majority of the beginner technology companies fall because of the blind belief of the team will never be able to meet the needs of their clients. When they asked me at the beginning of 2018: “Don’t you worry about creating a borrowing product and how difficult it is to position it on the market?” My answer was:

“We don’t have a reason to complain: we simply rush forward in the market, so we will already have a finished product by the time the market is worth using it.”

Today I know… if a startup says that, they are totally in the wrong way and if it doesn’t find the right path very quickly… Then the project can, unfortunately, be thrown out.

Most of the flipchart sheets from 2017 are still in my office to this day. Sometimes I tend to look at them nostalgically. It was a huge work with colleagues and co-founders, most of whom were replaced or dropped out over the past good three years. Every half-year, taking a strategic shift and performing a pivot… that’s all it takes for the team to get used to the new processes and start the new routine… everyone can rush back to the planning table. Unfortunately, this really isn’t for everyone.

After an impromptu startupper life anthology, maybe it’s time to weight the sides:

- INLOCK has found its identity in the year 2020. Our services consist of two products: Savings Account and Loan. Both products are spread widely and can be easily used by customers as they operate through simple and logical customer processes where decision points and situations that could stop the customer are reduced to near zero. At the service level, everything is handled intuitively and automatically.